Bubble-like borrowing. Is it a warning sign or a good idea?

It seems like the minute that the local real estate market starts to rise, home owners start feeling the call to spend their rising home equity. Some of this is folly; some is responsible use of available options.

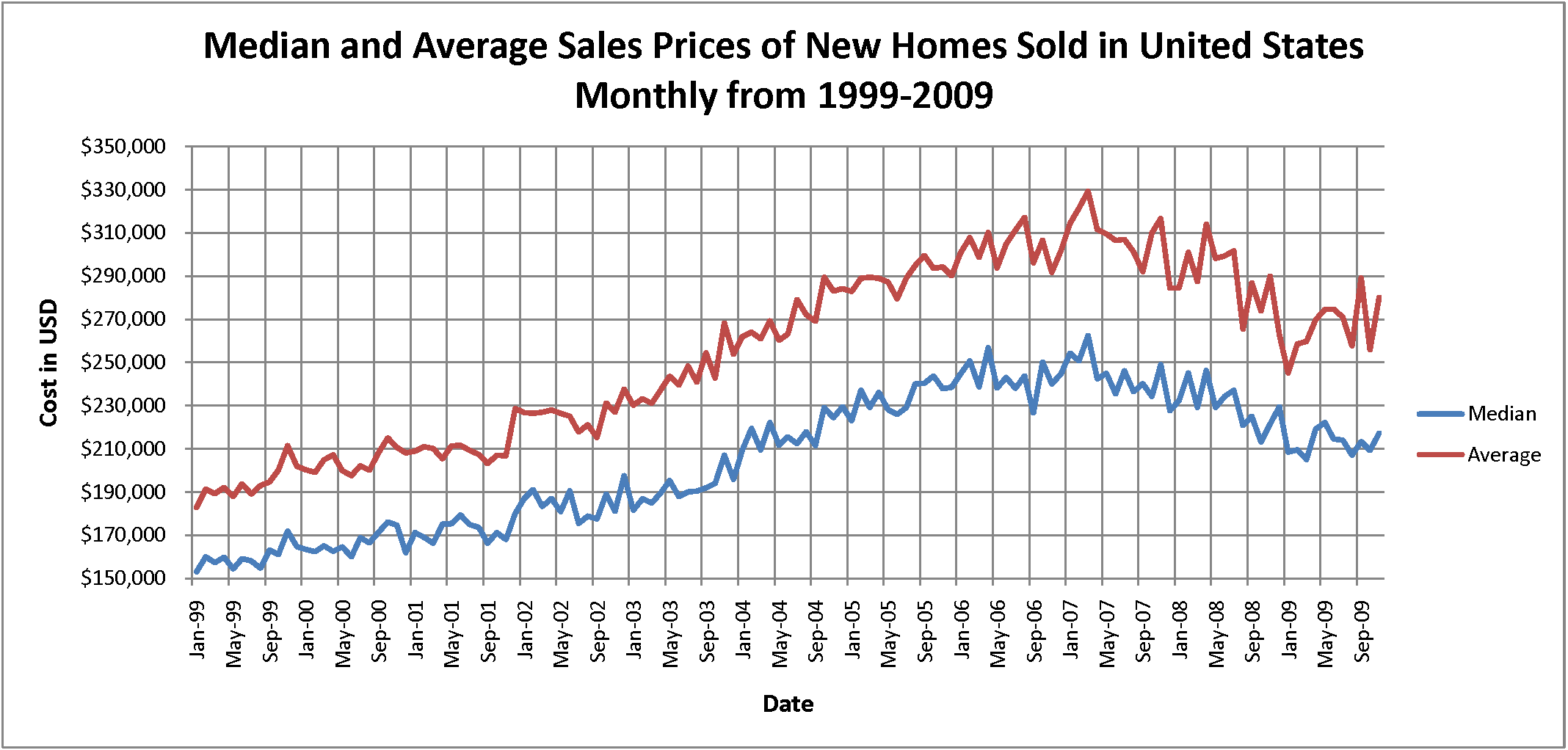

The real estate bubble burst between 2006-2008, with it went the wild lending practices that contributed to the number of underwater home owners. HELOCs were too easy to get and were based on bubble-level equity. When prices receded, owners found themselves underwater.

The result:

- Those who could not afford their mortgage payments were at risk of foreclosure.

- Those who intended to sell were stuck in their houses or were working with their lenders to do a short sale.

- Those who spent their equity on luxury items had nothing to show for it, except low equity in their house or negative equity. But, if they could still pay their mortgage, they were unharmed.

- Many people benefited by converting other debt into home equity debt. Home equity loans carry low, mortgage-level interest rates, around three percent. Student loans can be as high as eight percent. Credit card and other consumer debt is even higher. So, converting $100,000 in student loans into mortgage debt would reduce the payments (and spread them over a longer period.) As long as they could still pay their mortgage, they were unharmed.

- Other people benefited by financing home improvement during the housing boom. This put them in a better position to sell now that housing prices have recovered. If they did not plan to sell, then the improvements benefit them in their enjoyment of the changes. As long as they could still pay their mortgage, they were unharmed.

Now that home equity is high again, why are people so quick to put themselves into more debt?

HELOC borrowing dropped drastically as home equity went down. Now that home equity is going up, it is burning a hole in the pocket of home owners. The trend is repeating itself, according to The Boston Globe.

HELOC borrowing dropped drastically as home equity went down. Now that home equity is going up, it is burning a hole in the pocket of home owners. The trend is repeating itself, according to The Boston Globe.

If you are considering borrowing against your home equity, I advise you to keep an eye focused on your monthly debt payment, and also, the cost of what you are borrowing over the life of your mortgage.

Let’s go back to that $100,000 student loan. If it was a 10-year loan at eight percent, the monthly payment would be $1,213. The cost over ten years would total $145,560. If that student loan is converted into a 10-year HELOC at three percent, the monthly cost would be $966. The cost over the life of the mortgage would be $115,920. Were it a 15-year HELOC, the cost would be $691 monthly and $124,380 over the full term.

If you borrow $100,000 with a HELOC to redo your kitchen, change your windows, and go on vacation, you have increased your monthly debt by $966 a month for the next ten years ($115,920 total.) If you refinance your mortgage and add $100,000, that’ll cost $422 a month more for 30 years. That’s $151,920 if you stay in the house until the end of the mortgage.

If the borrower does not intend to sell the house and if the borrower is secure that the payment is not beyond their expected income, this is significant savings. Those are big ifs. Ten years is a long time. Please think before you turn your house into a piggy bank.